Martingale System for Greyhounds: Risks and Reality

Loading...

Contents

The Martingale system is the most famous betting strategy in the world, and it is famous for precisely the wrong reasons. The pitch is seductive: double your stake after every loss, and when you eventually win, you recover everything plus a profit equal to your original bet. It sounds foolproof. It is not. It is, in fact, one of the fastest routes to emptying a betting bank that has ever been devised, and the number of greyhound punters who have learned this the hard way is depressingly large. Find more strategy guides at greyhoundbettingsystem.

Yet the system persists. New bettors discover it every week, run it for a few sessions, enjoy the initial results, and then hit the losing streak that makes the mathematics impossible to sustain. Understanding why the Martingale fails is not just an academic exercise. It is a necessary inoculation against one of gambling’s most persistent bad ideas.

How the Martingale System Works

The mechanics are deceptively simple. You choose a selection method — backing the favourite, for instance — and place an initial stake. If the bet wins, you pocket the profit and start again at the base stake. If the bet loses, you double the stake on the next bet. You keep doubling after each loss until you win, at which point your winning bet recovers all previous losses and delivers a net profit equal to the original stake.

In a greyhound context, suppose you start with a two-pound stake on the favourite at even money. If it loses, your next bet is four pounds. If that loses, eight pounds. Then sixteen, then thirty-two. When you finally win, the payout covers all the accumulated losses plus that original two-pound profit.

The system relies on one assumption: that you will always eventually win a bet. For any single bet with a positive probability of success, this is technically true given infinite time and infinite money. The problem is that no punter has either of those things, and the gap between theoretical mathematics and practical reality is where the Martingale destroys betting banks with remarkable efficiency.

The appeal is psychological as much as mathematical. The Martingale produces frequent small wins punctuated by catastrophic losses. During the winning phases, which can last for days or weeks, the punter feels like the system is working perfectly. The steady drip of two-pound profits accumulates, confidence grows, and the next doubling sequence seems like a temporary inconvenience that will resolve itself. Then the losing streak arrives, and it arrives faster than most people expect.

The Mathematics of Failure

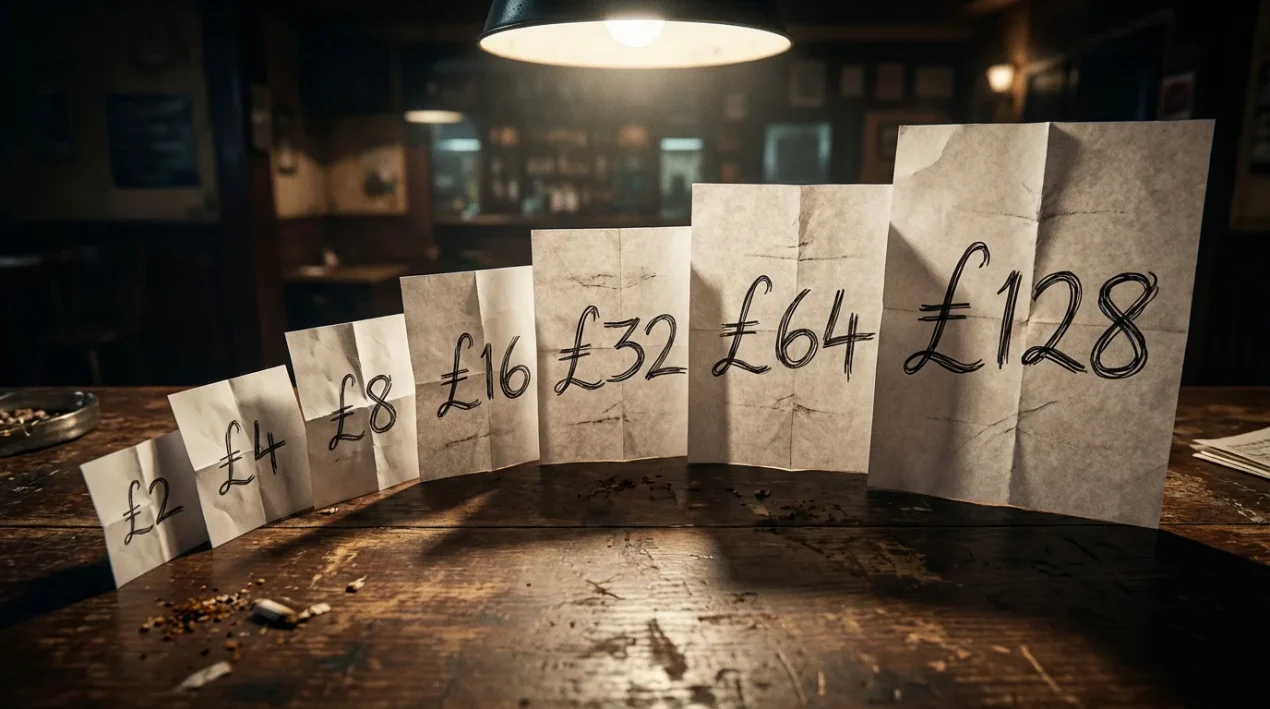

The fundamental problem with the Martingale is exponential growth. Doubling creates a sequence that accelerates far faster than human intuition anticipates. Starting from a two-pound base stake, six consecutive losses require the following progression: 2, 4, 8, 16, 32, 64. The seventh bet needs to be 128 pounds, and by this point the cumulative loss is 126 pounds. To recover that loss and make a two-pound profit, you need to risk 128 pounds on a single bet.

That ratio — risking 128 pounds to win 2 — is the Martingale laid bare. After seven losses, you are wagering 64 times your original stake for the same two-pound return. The risk-reward ratio has inverted so dramatically that the system is no longer a strategy. It is a desperate recovery attempt with catastrophic downside.

How likely is a seven-bet losing streak? More likely than most people think. If you are backing greyhound favourites at an average win probability of 33 percent, the probability of losing seven in a row is (0.67)^7 = approximately 6.1 percent. That means roughly one in every sixteen sequences will hit a seven-bet losing run. If you run four or five sequences per evening across several race meetings per week, you are virtually guaranteed to encounter this scenario within a few weeks of regular betting.

Extend the sequence further and the numbers become absurd. Ten consecutive losses — not unthinkable over a bad evening — would require a stake of 1,024 times the base amount. Starting from two pounds, that is a 2,048-pound bet to win two pounds. The cumulative loss at that point exceeds 2,000 pounds. No rational staking plan should ever produce a scenario where you risk four figures to recover a two-pound profit, yet the Martingale does exactly that with mechanical certainty given enough time.

Bookmaker limits add another layer of impossibility. Most bookmakers cap the maximum stake on individual greyhound races, and those caps will halt your doubling sequence well before you reach the theoretical recovery point. When the bookmaker stops you from placing the bet that would recover your losses, the Martingale has not just failed — it has failed with no path to recovery.

Safer Progressive Alternatives

If the Martingale’s core appeal — recovering losses through progressive staking — still resonates, there are systems that slow the escalation without eliminating risk entirely. None of them solve the fundamental problem of progressive staking, but they buy more time before the inevitable crisis point.

The Fibonacci system uses the Fibonacci sequence (1, 1, 2, 3, 5, 8, 13, 21…) instead of doubling. After a loss, you move one step up the sequence. After a win, you move two steps back. The escalation is slower than the Martingale, which means your bank survives longer during losing streaks, but the recovery from extended runs of losses is also slower and sometimes incomplete. Over a long enough period, the Fibonacci system faces the same terminal problem as the Martingale: stakes grow beyond what the bank or the bookmaker can support.

The D’Alembert system increases the stake by one unit after a loss and decreases it by one unit after a win. This is the gentlest of the progressive systems, with a much flatter escalation curve. The trade-off is that recovery from losing runs is extremely slow, and a sustained losing streak still accumulates significant losses even if individual bet increases are modest. The D’Alembert is less dramatic in its failure mode than the Martingale, but it is not safe.

The Labouchere system is more complex: you write a sequence of numbers, your stake is the sum of the first and last numbers, and you cross them off after a win or add the losing amount to the end after a loss. It offers more flexibility than the Martingale and the escalation is less aggressive, but the sequence can grow indefinitely during bad runs, creating the same fundamental problem in a more elaborate wrapper.

The honest assessment of all progressive staking systems is this: they redistribute when losses occur rather than preventing them. In a game where the bookmaker has a built-in edge, no staking pattern can convert a losing selection method into a profitable one. The selection must come first. The staking is secondary.

The Psychology Behind the Martingale

Understanding why the Martingale feels right even when the maths proves it wrong requires a brief detour into cognitive bias. The system exploits several psychological tendencies that punters are naturally susceptible to.

The gambler’s fallacy is the most obvious. After five losing bets, the human brain insists that a win must be due. It is not. Each greyhound race is an independent event. The probability of the favourite winning the sixth race is the same as it was for the first, regardless of the previous five results. The Martingale reinforces this fallacy by structuring the staking around the assumption that wins and losses must balance out, when in reality they are under no such obligation.

Loss aversion plays a role too. Once a punter is several steps into a Martingale sequence, the accumulated loss feels painful, and the desire to recover it becomes overwhelming. The rational response — accepting the loss and returning to the base stake — feels like giving up. Doubling the bet feels like taking action, like fighting back. The emotional pull towards the next doubling bet is powerful even when the intellectual case against it is clear.

Confirmation bias completes the picture. Punters who run the Martingale remember the sessions where the recovery bet landed and the losses were wiped clean. They forget, or downplay, the sessions where the sequence ran too deep and the bank took serious damage. The profitable evenings are treated as evidence that the system works. The catastrophic evenings are treated as bad luck rather than as the predictable, mathematically certain outcome of an unsustainable approach. Also explore our betting systems guide.

The Martingale is not a betting system. It is a loss-chasing mechanism dressed in mathematical clothing. It produces the illusion of control while systematically increasing your exposure to the exact outcome you are trying to avoid. The greyhound punters who build sustainable, long-term approaches to the sport are invariably those who abandon progressive staking in favour of flat stakes and better selection. The maths is not complicated. The discipline to accept it is the hard part.